Research

Papers, Posts & Appearances

Peer-reviewed publications, working papers, blog series, and academic talks from the RAIIS team.

The RAIIS engine is built on published research. These are the papers, working drafts, and talks that inform the calculation framework — the academic foundation behind every number Saladin produces.

Green Fees Series

A multi-part research series examining how ESG constraints affect portfolio performance and transaction costs.

Before the Green Fees: Why ESG Portfolio Management Isn't Straightforward

Unpacking the problem of inconsistent ratings, rising regulation, and performance uncertainty in ESG investing.

Green Fees: The Methodology Behind Measuring ESG Portfolio Impacts

A rigorous framework for assessing how sustainability screening affects performance and costs.

Papers & Publications

Peer-reviewed papers, working papers, and the PhD thesis behind the RAIIS Portfolio Management Framework.

Quantitative Finance · Taylor & Francis

Feature Configuration Effects in DRL Portfolio Management: A Risk-Focused Evaluation Under Market Stress

Examines how feature design choices shape deep reinforcement learning portfolio managers, with a focus on risk behavior under stressed market regimes.

Read paper →International Review of Financial Analysis · Elsevier

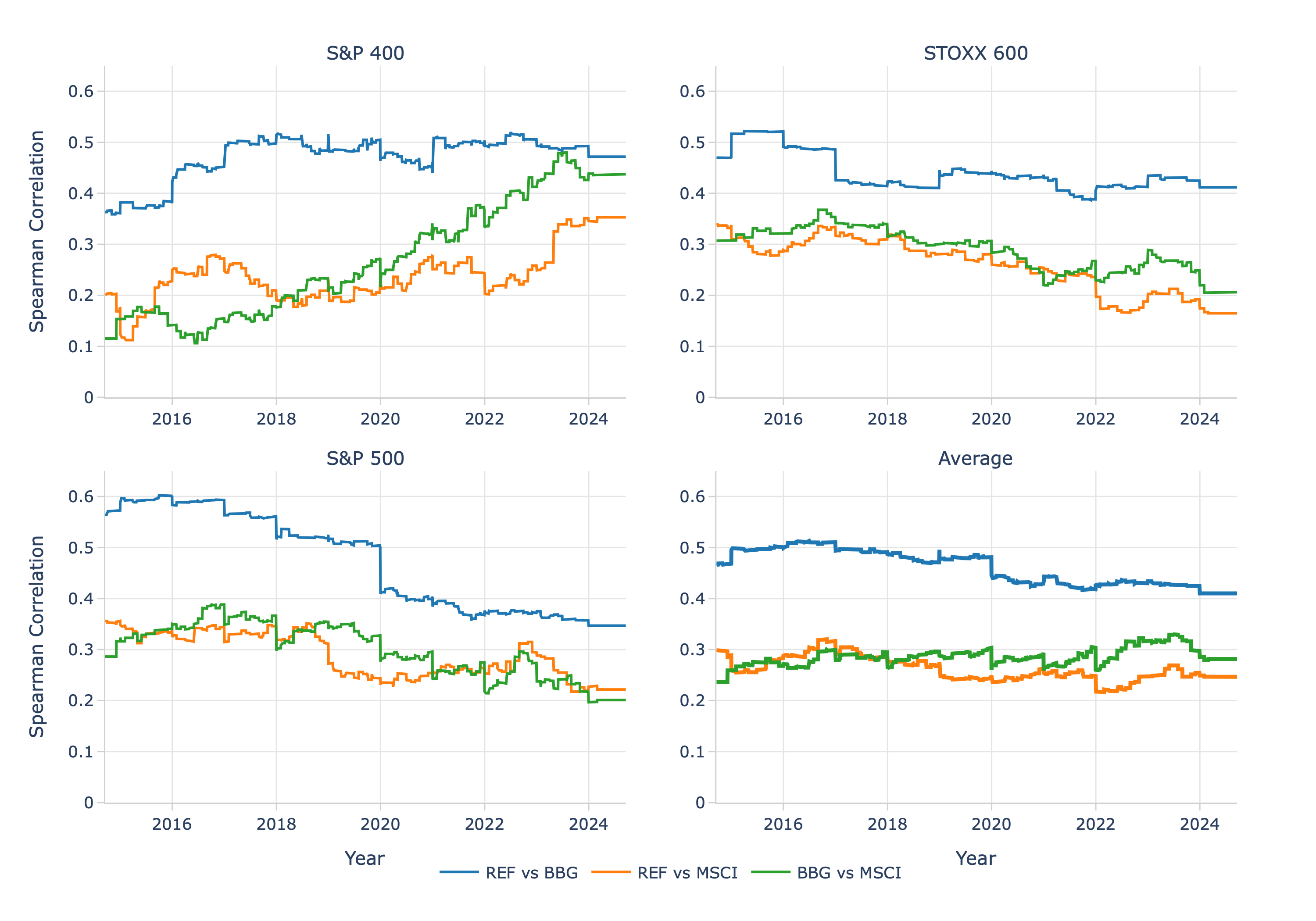

Green Fees: Sustainability Impacts on Portfolio Management

Quantifies how ESG screening and rating-provider choice affect portfolio performance and transaction costs across major equity universes.

Read paper →SSRN · Working Paper

Sectorial Analysis of ESG Features and Their Predictive Power

Identifies the ESG features that drive scores within and across sectors using a novel nested cross-validation framework on Refinitiv data for ~11k firms.

Read on SSRN →SSRN · Working Paper

ESG Rating Disagreement Dynamics and Stock Returns

Trains neural networks on four ESG providers for S&P 500 firms to predict rising disagreement; the predicted dynamics — not baseline levels — carry return-relevant information.

Read on SSRN →PhD Thesis · Zeppelin University

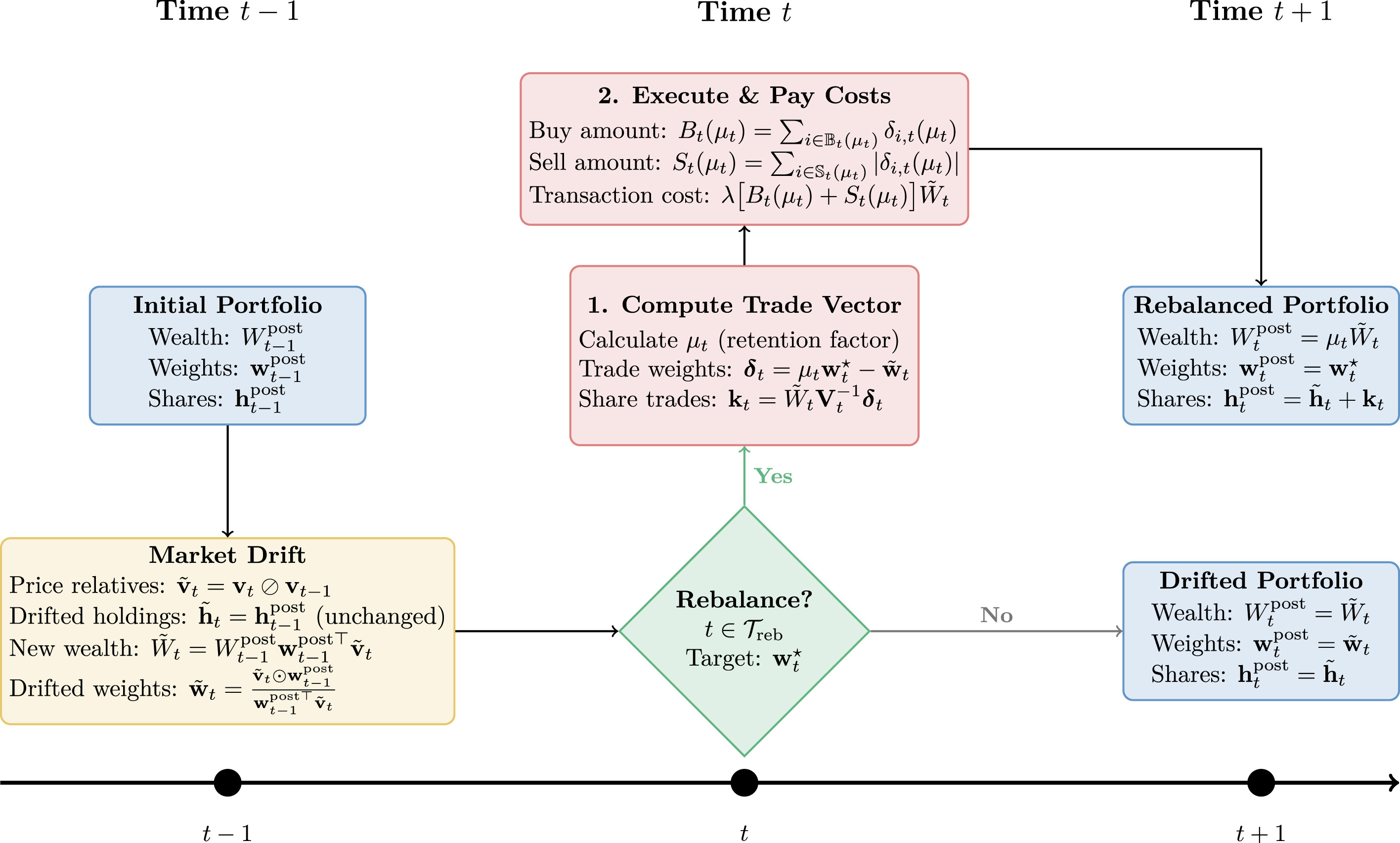

The PhD Thesis Behind the RAIIS Portfolio Management Framework (PMF)

Doctoral research at Zeppelin University that informed early thinking behind the RAIIS Portfolio Management Framework.

View thesis →Work in progress

A Ledger-Based Logic of Capital Flow · Alkan & Ayari

The founders' upcoming paper, taking a step beyond the dissertation. Details and a link will be posted here once available.

Conferences & Talks

Academic conferences and workshops where RAIIS research has been presented.

Energy, Climate & Finance Workshop — University of Duisburg-Essen

RAIIS presented work on sustainability impacts in portfolio management at the Energy, Climate & Finance Workshop hosted by the Chair of Energy Trading and Finance.

Open slide deck (PDF) →Technical Blog

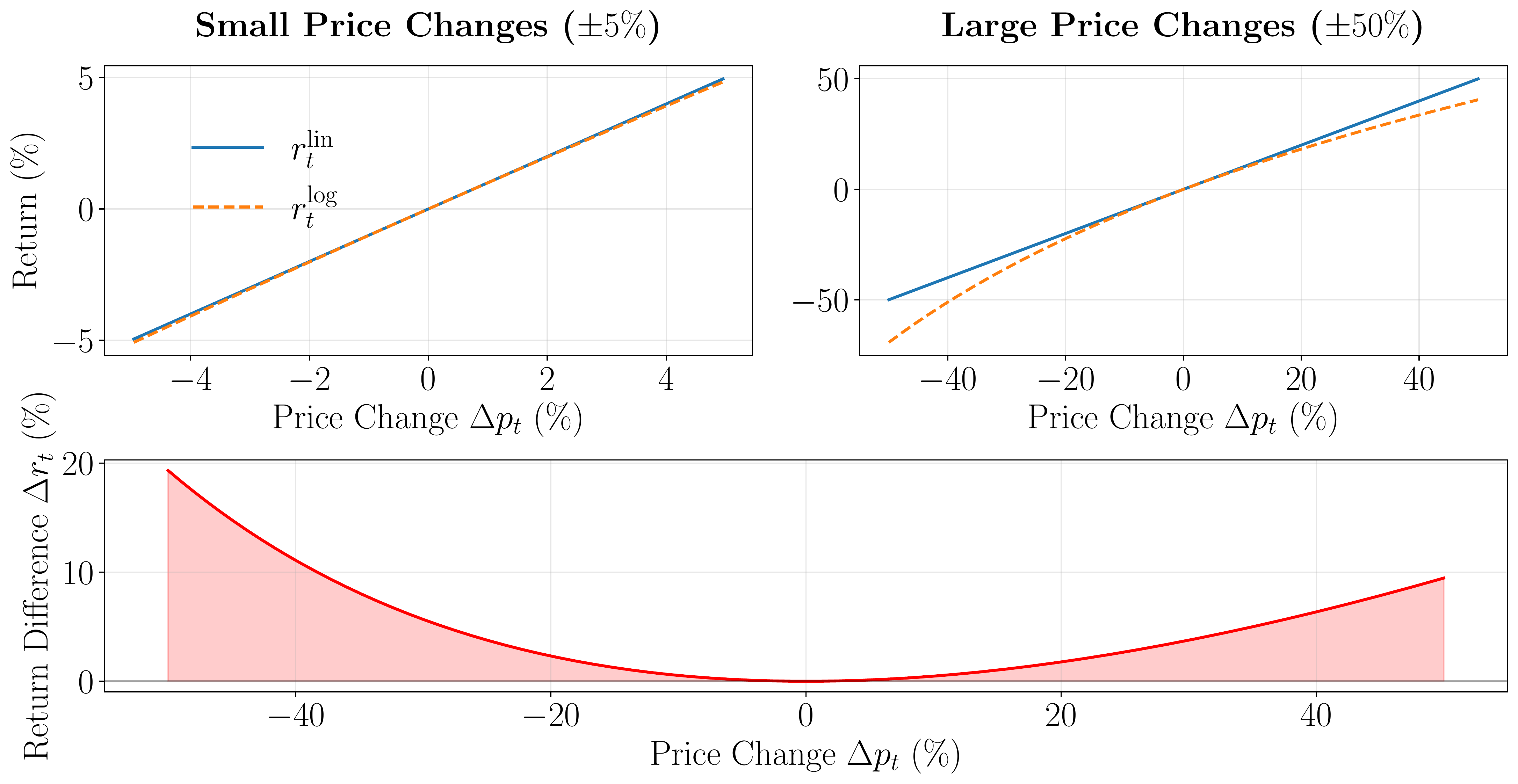

Portfolio Evaluation and Return Analysis

The mathematical framework for return analysis, comparing linear and logarithmic returns, and their practical implications for risk management.